When Goals Change Risk

Two years ago, I wrote about why I admire Ashvin Chhabra and his Wealth Allocation Framework. In particular, I was drawn to his idea that investors should separate their wealth into three portfolios: a Safety Portfolio, a Market Portfolio, and an Aspirational Portfolio. Rather than asking, “How do I maximize risk-adjusted returns?” Chhabra asks a more fundamental question: “What am I trying to accomplish?”

If you haven’t read it, you can find my earlier post on Ashvin Chhabra here.

Recently I came across a fascinating new paper, Gambling for Goals (Arkolakis et al., 2026), presented at this year’s NBER Summer Institute Household Finance meeting. It offers a compelling explanation for why speculative investing has become so common among younger households.

The authors argue that when major life goals such as homeownership, retirement, or upward mobility feel unattainable through conventional saving, people become more willing to take lottery-like financial bets. Using linked administrative data from Korea’s largest credit bureau, telecom provider, and credit card issuer, covering more than one million individuals, they find that people with difficult-to-reach goals are significantly more likely to engage in cryptocurrency investing. They also show that winning access to subsidized housing reduces cryptocurrency engagement by roughly 21 percent. Once an important goal becomes attainable, the desire to speculate declines.

The empirical findings are impressive and make clever use of a natural experiment to tease out causation, but what really captured my attention was the paper’s underlying assumption.

Economists usually model utility as smooth and continuous. If buying a particular house becomes impossible, buy a smaller one. If retiring at 65 is unrealistic, retire at 67. Wealth increases gradually, and utility increases gradually alongside it.

Human psychology often works differently. Many of the goals we care about are experienced as thresholds, not gradients.

You are either a homeowner or a renter.

You are financially independent or you still need to work.

You made partner or you didn’t.

You started your own company or you never did.

You crossed $1 million in net worth or you haven’t.

These thresholds are often socially constructed, but that does not make them any less psychologically meaningful. We naturally organize our lives into categories, even when the underlying variable, wealth, is continuous.

Once you accept this premise, a great deal of speculative investing becomes easier to understand.

If someone believes disciplined saving will never allow them to cross an important threshold, then a lottery-like investment may represent the only perceived path. The question is no longer, “What has the highest expected risk-adjusted portfolio return?” It becomes, “What gives me any realistic chance of reaching the life I want?”

That observation immediately reminded me of Chhabra.

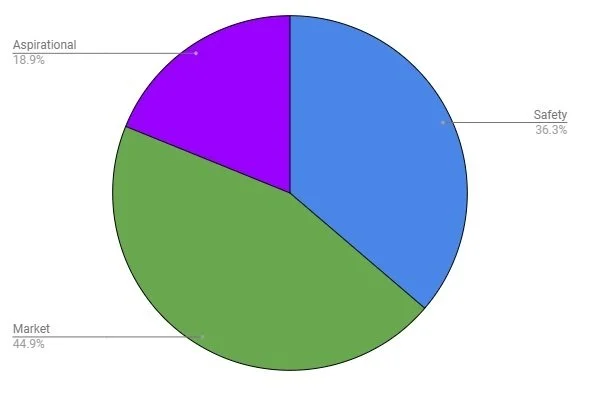

His Aspirational Portfolio is designed precisely for transformational opportunities: concentrated stock positions, entrepreneurship, venture capital, or other asymmetric investments capable of changing one’s financial trajectory. But unlike the behavior described by Arkolakis et al., Chhabra insists that these bets remain contained. The Safety Portfolio protects essential goals. The Market Portfolio compounds wealth efficiently. Only the Aspirational Portfolio pursues extraordinary outcomes.

Viewed together, I think these ideas complement one another remarkably well.

Arkolakis et al. explain why investors become attracted to transformational bets.

Chhabra explains how they should pursue them.

The former is a positive theory of investor behavior. The latter is a normative framework for portfolio construction.

The paper doesn’t claim that difficult-to-reach goals explain all speculative investing, nor do I think the evidence supports that conclusion. In what I found to be one of the paper’s most convincing exercises, the authors study individuals who win access to subsidized housing through Korea’s housing lottery. Winning reduces cryptocurrency engagement by roughly 21 percent, a meaningful decline, but far from eliminating speculative behavior.

I actually view that as a strength rather than a weakness.

Had cryptocurrency engagement fallen by 80 percent, I would have wondered whether the authors were attributing far too much to a single mechanism. Instead, the results suggest that aspirations are one important driver of speculative investing alongside many others. Some investors are motivated by optimism or entertainment. Others may be attracted to characteristics unique to cryptocurrencies themselves, including their potential diversification benefits, their role as a non-sovereign store of value, or the ability to hold assets that are resistant to censorship or confiscation. The paper’s contribution is not to explain every reason someone might own crypto. Rather, it identifies an important and previously underappreciated motive: when meaningful life goals feel out of reach, people become more willing to pursue lottery-like investments.

That, in turn, brings me back to Chhabra. If investors naturally seek transformational outcomes, simply telling someone to “buy the index” may miss an important psychological reality. If someone genuinely believes conventional investing cannot achieve their most important life goals, they will almost certainly seek speculation somewhere else.

Chhabra’s insight is that this impulse doesn’t need to dominate the entire portfolio. By deliberately allocating a limited portion of wealth to an Aspirational Portfolio, investors can pursue transformational opportunities while protecting the capital needed to achieve their core financial objectives.

Perhaps speculative investing has become more common not because people have become less rational, but because conventional paths to achieving psychologically meaningful goals have become less convincing.

The challenge, then, isn’t to eliminate aspiration. Aspiration is one of the great drivers of human progress. The challenge is to channel it wisely: to build a portfolio that allows us to pursue transformational dreams without jeopardizing the financial security we’ve worked so hard to achieve.